Why the Best Personalized Finance Apps Are Actually Relationship Tools

Stop arguing over grocery runs. Discover how the latest personalized finance apps are evolving into relationship tools that manage household energy, not just transactions and budgets.

Beyond Budgeting: Why the Best Personalized Finance Apps Are Actually Relationship Tools

You've got the budget locked down. The bills are on autopilot. Your savings rate would make a financial advisor weep tears of joy. So why are you still arguing about that $40 grocery run?

Because most personalized finance apps treat money like it exists in a vacuum. They categorize, track, and alert. They're built for the individual, not the partnership. And if you're in a relationship, that's a problem.

The best personalized finance apps in 2026 aren't just managing your money. They're managing your relationship's energy. They understand that the question "Can we afford this?" isn't purely mathematical. It depends on timing, context, and whether you're asking during a high-stress week or a calm Sunday morning.

This guide breaks down how modern personalized finance apps are evolving beyond transaction tracking into relationship tools. You'll learn which apps understand partnership dynamics, how to choose one that reduces friction instead of creating it, and why "personalization" now means context awareness, not just custom categories.

VibeCheck App

Know what she needs. Before she has to say it.

Track her cycle, understand her phases, be the partner she deserves.

Download Free on iOS →Table of Contents

- The Modern Partner's Dilemma

- Competitive Matrix: Top Personalized Apps for Couples

- The "Sync" Factor: Why Context Matters More Than Categories

- 3 Ways a Personalized App Makes You a Better Partner

- How to Choose the Right Personalized Finance App for Your Relationship

- Frequently Asked Questions

The Modern Partner's Dilemma

You want to lead the financial strategy without becoming the household auditor. Most finance apps force you to choose between being hands-off or micromanaging.

You're 32. You've been together three years. You handle the bills because you're better with numbers, or maybe because she asked you to, or maybe because someone had to and you stepped up. Either way, you're now the de facto CFO of a two-person household.

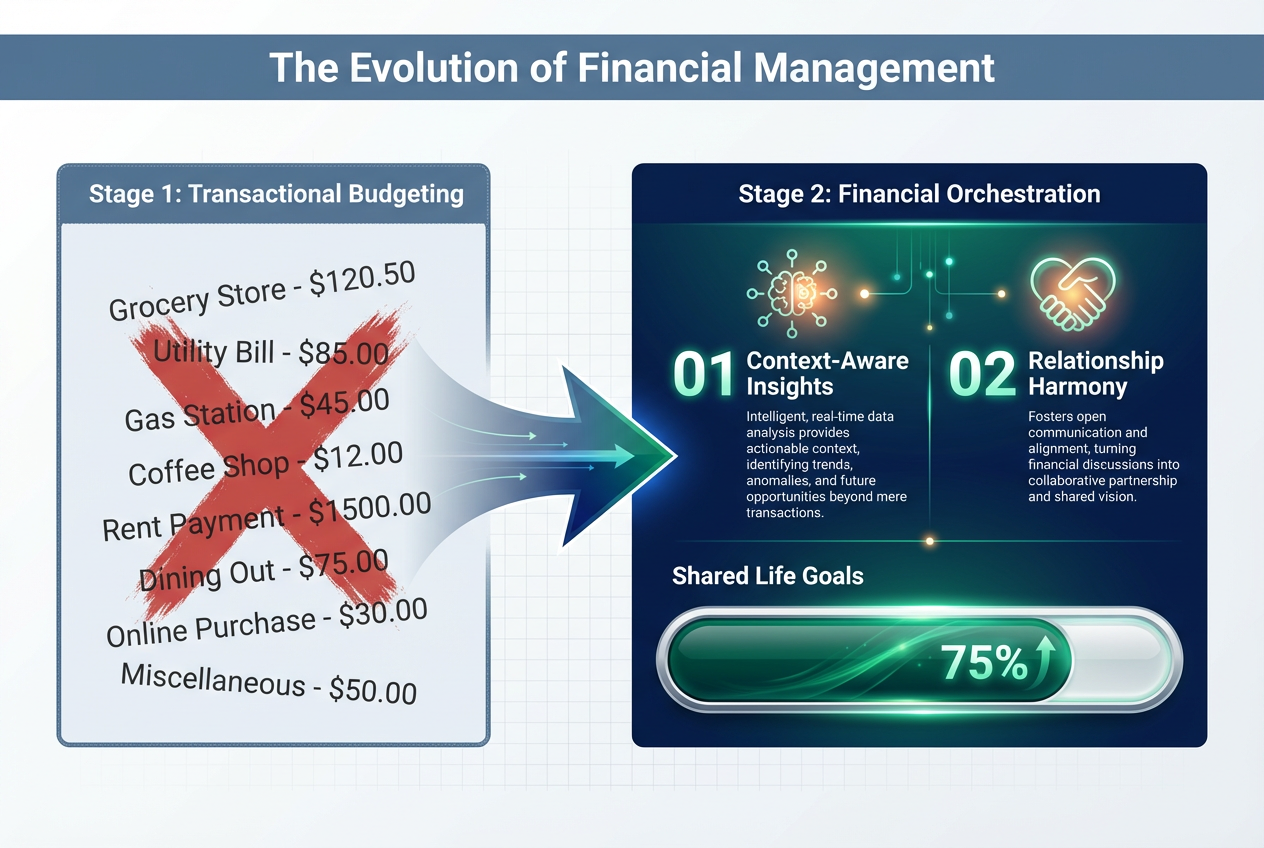

The problem? Most personalized finance apps turn you into an accountant, not a partner.

They send alerts at terrible times. They flag spending that needs context (yes, that $80 was for her sister's birthday gift, not a spontaneous splurge). They create a power dynamic where one person "monitors" and the other feels monitored.

Move from manual expense tracking to automated financial orchestration. A truly personalized app provides the context needed to manage shared goals without the administrative burden.

Move from manual expense tracking to automated financial orchestration. A truly personalized app provides the context needed to manage shared goals without the administrative burden.

The modern man's financial dilemma isn't about making money. It's about managing money without creating relationship friction. You need a system that:

- Tracks spending without judgment

- Provides insights without nagging

- Allows shared visibility without shared spreadsheets

- Reduces the mental load instead of adding to it

Traditional budgeting apps optimize for the individual. They assume every dollar decision happens in isolation. They don't account for the fact that bringing up the credit card balance on a stressful Wednesday hits differently than discussing it over a relaxed weekend brunch.

This is where personalized finance apps are evolving. The best ones in 2026 understand that personalization isn't just about custom spending categories. It's about understanding the rhythm of your household, the timing of financial conversations, and the emotional weight of money decisions.

If you're tired of being the money police in your relationship, you're not alone. The gap between "good with money" and "good at talking about money with your partner" is where most relationships struggle. The right app closes that gap.

Competitive Matrix: Top Personalized Apps for Couples

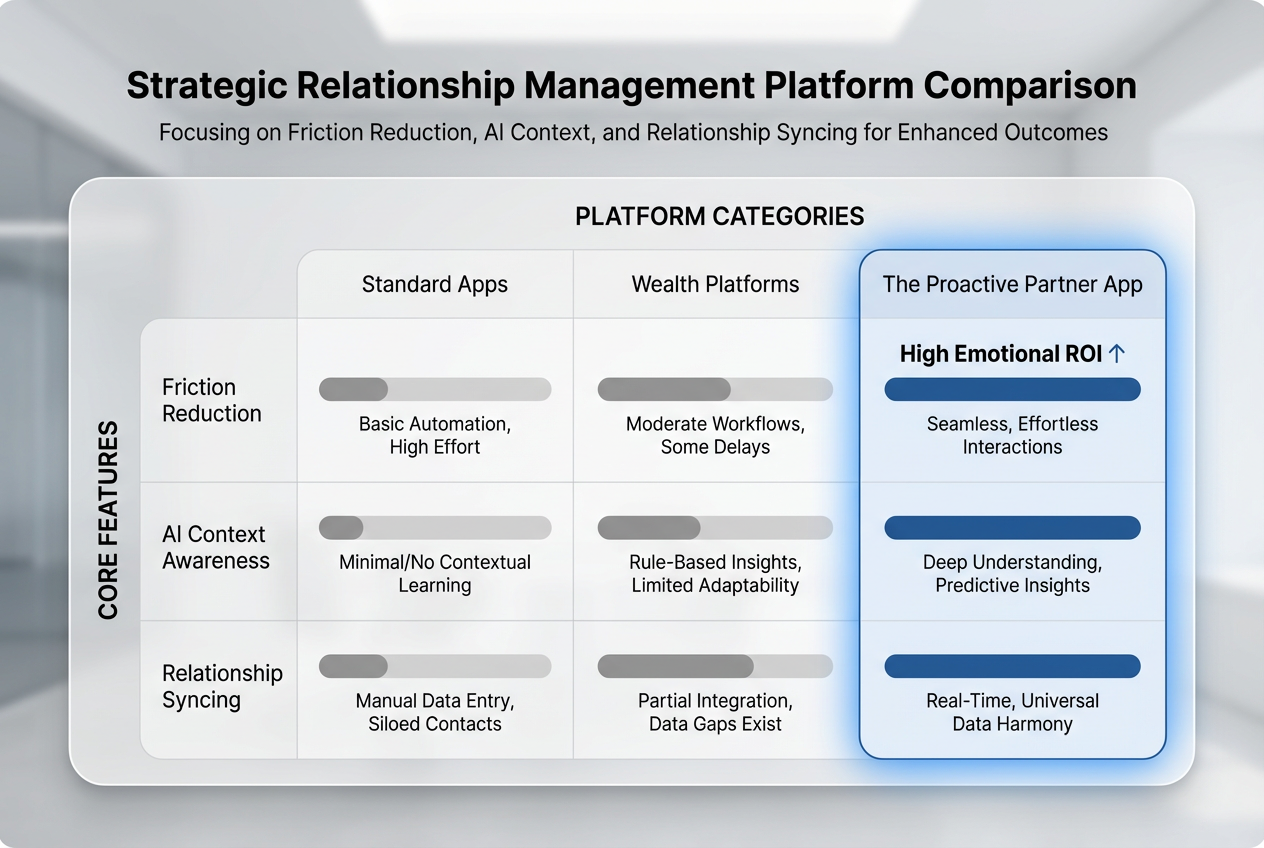

The finance app landscape splits into three camps: analytical powerhouses that feel like work, simple trackers that lack depth, and emerging relationship-aware platforms that understand partnership dynamics.

Not all personalized finance apps understand couples. Here's how the top contenders stack up when you're managing money as a team, not just as an individual.

Not all finance apps are built for partners. This matrix evaluates how top-tier apps handle the emotional and practical nuances of shared household financial management.

Not all finance apps are built for partners. This matrix evaluates how top-tier apps handle the emotional and practical nuances of shared household financial management.

Monarch Money: The Power Couple's Dashboard

What it does well: Monarch treats "Partner Mode" as a first-class feature, not an afterthought. You both get full visibility without constant check-ins. The shared goals feature actually shows progress visually, which matters more than you'd think.

Where it falls short: It's analytical to a fault. Every screen feels like a board meeting. If your partner isn't naturally numbers-driven, the interface becomes a barrier instead of a bridge. Monthly cost runs $15-$20, which is reasonable for what you get but adds up annually.

Best for: Couples who are both financially engaged and want a comprehensive wealth dashboard.

Origin: The Long Game

What it does well: Origin connects daily spending to long-term planning. Budgets flow into tax projections, which feed estate planning, which link to retirement goals. It's the most holistic view available.

Where it falls short: It assumes you're already wealthy or well on your way. The interface targets "power couples" building generational wealth, which can feel intimidating if you're just trying to stop fighting about the grocery budget. Pricing is steep at $200+ annually.

Best for: High-earning couples focused on wealth building across multiple accounts and asset types.

Honeydue: The Minimalist's Choice

What it does well: Dead simple. Track bills, split expenses, send "I owe you" notes. No learning curve. Free to use with basic features.

Where it falls short: It's 2019 tech in a 2026 market. Zero AI insights. No predictive features. Lacks the "personalized" depth that men in this age bracket expect from modern apps. It's a shared ledger, not a financial advisor.

Best for: Couples just starting to combine finances who need basic tracking without complexity.

VibeCheck + Finance Integration: The Relationship-First Approach

What it does well: This is where the market is heading. Apps that understand relationship dynamics first, financial management second. VibeCheck started as a relationship app for men that helps partners understand cycles and timing. The finance integration angle? Knowing when to have money conversations based on energy levels and stress cycles.

Where it falls short: Still emerging. Not as feature-complete as dedicated finance platforms for pure transaction tracking.

Best for: Men who want to lead financial planning without creating relationship friction. Particularly effective if you're already using relationship timing tools.

The Comparison Table

| Feature | Monarch | Origin | Honeydue | Relationship-First Apps |

|---|---|---|---|---|

| Partner visibility | Excellent | Good | Basic | Contextual |

| AI insights | Good | Excellent | None | Relationship-focused |

| Visual progress tracking | Excellent | Good | Basic | Strength-based |

| Friction reduction | Medium | Low | Medium | High |

| Monthly cost | $15-20 | $17-20 | Free | $10-15 |

| Learning curve | Medium | High | Low | Low |

| Context awareness | Low | Low | None | High |

The gap in this market? No mainstream finance app currently integrates the timing of financial conversations with relationship dynamics. They'll tell you what you spent. They won't tell you that bringing up a budget review when she's in her luteal phase is a tactical error.

For men who want to be proactive partners, not reactive accountants, understanding relationship timing matters as much as understanding cash flow.

The "Sync" Factor: Why Context Matters More Than Categories

Most apps personalize based on your spending patterns. The best ones personalize based on your life patterns. There's a difference between knowing what you spend and knowing when to talk about it.

Here's what traditional "personalized" finance apps do: They learn you spend $200 monthly on groceries, $50 on gas, $80 on restaurants. They categorize. They alert when you're over budget. They optimize spending categories.

Here's what they don't do: Understand that financial stress isn't evenly distributed across the month.

Every relationship has cycles. High-energy weeks and low-energy weeks. Seasons of growth and seasons of consolidation. Times when money conversations flow easily and times when the same discussion becomes a minefield.

The "Sync" factor is about temporal intelligence. A truly personalized finance app doesn't just track what you spend. It understands the rhythm of your household.

Three Dimensions of Financial Synchronization

1. Emotional Bandwidth

You know this intuitively. There are weeks when you can have a strategic conversation about retirement contributions and it feels productive. There are weeks when asking about a $40 transaction feels like an accusation.

Apps with sync intelligence recognize this. They don't blast alerts during high-stress periods. They surface insights during calm windows. They understand that the best time to discuss a spending change is not immediately after the transaction.

2. Life Stage Alignment

Your financial priorities shift throughout the year. January brings insurance renewals and tax planning. Summer brings vacation spending. December brings holiday budgets and year-end bonuses.

But beyond the calendar, your relationship has its own seasons. Times of building, times of maintaining, times of pivoting. A synced app recognizes these patterns and adjusts its recommendations accordingly.

3. Goal Synchronization

Most couples have mismatched financial timelines. One person is focused on the next vacation. The other is worried about retirement. Both are valid, but they're operating on different frequencies.

Apps that understand sync help align these timelines. They show how the short-term decisions support long-term goals. They make the abstract concrete with visual progress indicators.

Why This Matters for Men in Relationships

You're trying to be a proactive partner. You want to lead the financial planning without being the bad guy who always says "we can't afford that."

The difference between a good finance app and a great one is context awareness. A good app tells you you're over budget. A great app helps you frame that conversation constructively.

If you're already using tools to understand your partner better, extending that awareness to financial conversations is the natural next step.

The apps winning in 2026 aren't the ones with the most features. They're the ones that reduce cognitive load. They handle the "what" automatically so you can focus on the "when" and "how" of financial partnership.

3 Ways a Personalized App Makes You a Better Partner

The best apps don't just manage money. They manage the relationship dynamics around money by removing friction, providing clarity, and reducing mental load.

Shift the conversation from "What did we spend?" to "Look what we've built." Strategic visuals like progress bars help partners focus on long-term wins over daily friction.

Shift the conversation from "What did we spend?" to "Look what we've built." Strategic visuals like progress bars help partners focus on long-term wins over daily friction.

1. Removes the "Audit" Vibe

The worst part of being the household CFO? Feeling like you're constantly questioning your partner's spending decisions.

"What was this $60 charge?" "Why did we spend $150 at Target again?" "Can you explain these transactions?"

These questions are necessary for financial awareness. They're also relationship poison when they become frequent.

A properly personalized finance app eliminates audit culture through:

Automatic categorization with intelligence. Modern apps don't just label transactions. They understand context. That $80 wasn't "miscellaneous spending." It was your partner's sister's birthday gift. The app knows because it learned the pattern.

Shared visibility without shared interrogation. Both partners can see everything without needing to ask. Questions become about strategy ("Should we reallocate our restaurant budget to savings?") instead of tactics ("What did you buy?").

Proactive alerts to both partners. When you're approaching a budget limit, both of you know. It's not one person monitoring the other. It's the system informing the team.

This matters because the partner who "manages" the money often becomes the perceived bad guy. Removing that dynamic is worth the monthly subscription alone.

2. Proactive Goal Setting Creates Shared Wins

Most budget apps focus on limits. "You've spent 80% of your dining budget." "You're over your clothing limit."

Limit-based thinking creates a scarcity mindset. Every dollar spent feels like a loss. Every purchase requires justification.

The best personalized apps flip this. They focus on progress, not limits.

Visual progress indicators matter. Seeing a retirement account progress bar move from 23% to 24% funded feels different than reading a balance increase from $187,450 to $190,200. Both show the same information. One creates emotional momentum.

Milestone celebrations become shared. When you hit a savings goal, the app acknowledges it. Small wins compound. Celebrating $5,000 in your emergency fund builds enthusiasm for the next $5,000.

Future-focused conversations replace past-focused ones. Instead of "Why did we spend so much last month?" you're discussing "If we reduce restaurant spending by $100 monthly, we'll hit our vacation goal three months earlier."

This transforms you from the money police to the guy with the plan. You're not restricting. You're enabling.

For men who want to be better partners in practical ways, showing progress beats discussing problems.

3. Cognitive Load Reduction: The Hidden Superpower

The mental burden of financial management isn't just tracking expenses. It's:

- Remembering bill due dates

- Monitoring multiple accounts

- Catching unusual charges

- Updating budgets as life changes

- Coordinating with your partner on major purchases

- Planning for irregular expenses (car maintenance, holiday gifts, annual subscriptions)

This cognitive load is invisible until it's gone.

A truly personalized app handles the mental work:

Predictive alerts for upcoming expenses. It knows your car registration is due in two weeks because it saw the charge last year. It reminds you before, not after.

Automatic adjustment for irregular income. Freelancer? Commission-based? The app learns your income pattern and adjusts budget recommendations accordingly.

Intelligent categorization that improves over time. You're not constantly recategorizing transactions. The AI learns that Costco purchases split between groceries and household items based on the total.

The superpower here? Being the partner who "has it handled" without actually handling every detail manually. You're providing leadership through systems, not micromanagement.

This is particularly valuable if you're the partner who naturally takes on the planning role. Understanding what your partner needs includes removing unnecessary stress, and financial anxiety is a top relationship stressor.

How to Choose the Right Personalized Finance App for Your Relationship

The best app isn't the one with the most features. It's the one that matches your relationship dynamics, technical comfort level, and financial complexity.

Choosing a personalized finance app when you're in a relationship requires different criteria than choosing one as an individual. Here's the framework that actually matters.

Start With Your Relationship's Financial Complexity

Low Complexity: Shared bills, simple accounts

- You split rent and utilities

- Each person maintains their own accounts

- Few shared financial goals beyond immediate expenses

Best fit: Honeydue or similar simple tracking apps. You don't need full wealth management. You need easy expense splitting and bill reminders.

Medium Complexity: Mostly combined finances

- Joint checking, maybe separate savings

- Shared goals (house down payment, vacation fund)

- Some investment accounts

- You coordinate on major purchases

Best fit: Monarch Money. You need visibility, goal tracking, and the ability to see the full financial picture without excessive complexity.

High Complexity: Fully integrated household

- Multiple investment accounts

- Real estate holdings

- Tax optimization strategies

- Estate planning considerations

Best fit: Origin or equivalent comprehensive platforms. You need the integration across accounts, tax implications, and long-term planning tools.

Assess Your Partner's Financial Engagement Level

This is the variable most people ignore and the one that determines success or failure.

If your partner is highly engaged:

- Any full-featured app works

- Focus on functionality and features

- Complexity isn't a barrier

If your partner is moderately engaged:

- Prioritize clean interface over feature depth

- Look for apps with good mobile experience

- Visual progress tracking becomes essential

- Consider apps that integrate with relationship timing tools to reduce friction around money conversations

If your partner prefers you handle it:

- Avoid apps that require dual input

- Focus on apps with excellent reporting you can share

- Prioritize apps that create summaries over raw data

- Consider relationship-first platforms that help you communicate financial information constructively

The engagement level mismatch kills more app adoptions than feature gaps. An app requiring both partners to categorize transactions will fail if one person isn't willing to do the work.

Key Features That Actually Matter for Couples

Non-negotiable:

- Shared account access with appropriate permissions

- Mobile app for both iOS and Android

- Automatic transaction syncing (manual entry always fails)

- Secure bank-level encryption

High value:

- Visual goal tracking

- Customizable budget categories

- Bill payment reminders

- Spending insights and trends

- Net worth tracking

Nice to have:

- Custom reports

- Receipt capture

- Investment tracking

- Tax optimization tools

- Integration with other financial services

The Questions to Ask Before Choosing

1. Does this app reduce or increase relationship friction? If setting it up requires a three-hour conversation about spending philosophy, it's adding friction. The best apps allow you to start simple and add complexity as needed.

2. Can we both access it without constant coordination? Apps requiring one person to "share" information with the other create a power dynamic. Look for true multi-user support.

3. Does the interface make sense to my partner? Open the app. Show your partner. Can they understand the main dashboard in 30 seconds? If not, adoption will fail.

4. What happens if we stop actively managing it? The best apps provide value even during low-engagement periods. Automatic tracking and basic insights should continue working without manual input.

5. How does it handle irregular income or expenses? If your income varies or you have significant irregular expenses (annual insurance, quarterly taxes, holiday spending), the app needs to handle this intelligently.

Trial Period Strategy

Don't commit to annual subscriptions immediately. Most apps offer 30-day trials or money-back guarantees.

Week 1: Set up accounts and connect banks. Evaluate ease of setup.

Week 2: Use it passively. Let transactions accumulate. Check if automatic categorization works.

Week 3: Create a shared goal. Test the goal-tracking interface. See if it motivates or annoys.

Week 4: Have a financial conversation using the app's data. Does it make the discussion easier or harder?

If you make it through four weeks and both partners are still using it, you've found a winner.

The Integration Consideration

The cutting edge? Apps that integrate financial management with relationship intelligence.

If you're already using tools to understand your partner's cycle and energy patterns, finding a finance app that respects those patterns creates a powerful system.

The timing of financial conversations matters as much as the content. An app that helps you choose when to discuss money, not just what to discuss, represents the next evolution of personalized finance tools.

Ready to actually understand her?

Join thousands of men using VibeCheck to track her cycle and show up better every day.

Frequently Asked Questions

What is a personalized finance app?

A personalized finance app uses AI and machine learning to understand your specific spending patterns, financial goals, and household dynamics. Unlike basic budgeting apps that simply categorize transactions, personalized apps learn your behavior over time and provide context-aware insights tailored to your situation. For couples, the best personalized finance apps recognize relationship dynamics and help reduce friction around money conversations by providing shared visibility and intelligent recommendations.

Can two people use the same finance app?

Yes, most modern finance apps support multiple users with varying permission levels. Apps like Monarch Money and Origin offer dedicated "partner mode" features allowing both people to access accounts, view transactions, and track shared goals. The key is choosing an app designed for couples rather than forcing a single-user app to work for two people. Look for features like joint goal tracking, shared budgets, and the ability for both partners to receive alerts and notifications.

How much should I pay for a personalized finance app?

Quality personalized finance apps for couples typically range from free (basic features) to $15-20 monthly for comprehensive platforms. Honeydue offers free basic tracking. Monarch Money runs $15-20 monthly. Origin costs approximately $200 annually. The right price depends on your financial complexity and how much value you place on reducing relationship friction around money. For many couples, paying $15 monthly to eliminate arguments about finances provides significant ROI. Consider the subscription cost against the money you'll save through better financial decisions and the relationship stress you'll avoid.

What's the difference between a budget app and a personalized finance app?

Budget apps track spending and compare it to predetermined limits. Personalized finance apps go deeper by learning your patterns, predicting future expenses, and providing context-aware insights. A budget app alerts you when you've exceeded your restaurant budget. A personalized app recognizes you spend more on dining during stressful work weeks, adjusts expectations accordingly, and might suggest reallocation strategies that fit your lifestyle. For couples, personalized apps understand household dynamics and help time financial conversations appropriately rather than sending alerts that create conflict.

Do finance apps really help relationships?

Research shows financial stress is a leading cause of relationship conflict, and finance apps can significantly reduce this stress when chosen and implemented properly. Apps work best when they reduce the "audit" dynamic by providing shared visibility, shift focus from limits to progress through goal tracking, and decrease mental load by automating routine financial management tasks. The key is choosing an app that matches both partners' engagement levels. Apps requiring equal input from both partners fail if one person isn't financially engaged. For men seeking to be proactive partners, the right finance app transforms you from money police to strategic planner.

Can a finance app integrate with relationship apps?

This is an emerging trend in 2026. While traditional finance apps operate independently, relationship-aware platforms are beginning to consider emotional and biological cycles in financial planning. Apps like VibeCheck, which help men understand their partner's hormonal cycles and energy patterns, can inform the timing of financial discussions. The principle is simple: knowing when your partner has high emotional bandwidth for financial planning conversations increases the likelihood of productive outcomes. As this space evolves, expect more integration between relationship intelligence tools and financial management platforms.

What should couples track in a finance app?

Essential tracking for couples includes shared expenses (rent, utilities, groceries), individual discretionary spending, joint savings goals (emergency fund, house down payment, vacation), debt payoff progress, and net worth trends. Advanced users might track investment performance, tax optimization opportunities, and estate planning elements. Start simple with basic income and expense tracking, then add complexity as you build the habit. The mistake most couples make is trying to track everything immediately, which creates unsustainable administrative burden. A good personalized app grows with you, starting simple and adding features as your financial sophistication increases.

How do I convince my partner to use a finance app?

Lead with the benefit to them, not the benefit to the household budget. Instead of "We need to track our spending better," try "I want to find a way to manage our money that doesn't require us to have stressful conversations every time something unexpected comes up." Frame the app as a tool that reduces questions and increases freedom rather than one that monitors spending. Consider starting with a simple app focused on shared goals rather than expense tracking. Show progress toward a goal they care about (vacation fund, home renovation, debt payoff) to build engagement. If your partner responds better to certain communication styles, use that knowledge when introducing the app concept.

Most personalized finance apps are built for individuals who happen to be in relationships. The best ones are built for relationships that happen to need financial management.

The difference matters. One optimizes for your bank account. The other optimizes for your partnership.

If you're tired of being the money police, if financial conversations consistently derail into arguments, or if you want to be the proactive partner who has a plan without becoming the controlling partner who monitors every dollar, the right personalized finance app changes the dynamic.

The future of financial apps isn't just AI-powered categorization or predictive analytics. It's relationship intelligence. It's understanding that money management is inseparable from partnership dynamics, and the timing of conversations matters as much as the content.

Choose an app that reduces friction, provides clarity, and helps you lead without micromanaging. That's personalization that actually matters.

Tags

Related Articles

Continue reading to deepen your understanding

The Strategic Partner’s Guide to Planning an Engagement Around Her Cycle

Don’t leave your proposal to chance. Learn how her biological rhythm impacts emotional receptivity and how to align your big question with the phase where she feels her best.

How to Plan Weekend Trips Around Your Girlfriend’s Cycle: A Tactical Guide

Stop booking trips that end in friction. Learn how to map weekend travel to her biological phases to reduce friction by 41% and maximize your time together.

How to Plan Engagement Around Girlfriend Cycle Timing

Master how to plan engagement around girlfriend cycle timing to leverage an 800% estrogen spike and ensure a joyous yes with our 4-phase tactical guide.

How to Apologize to Your Girlfriend After a Fight: The Bio-Intelligent Timing Guide

Stop making fights worse with mistimed apologies. Learn the science of the 20-60 minute repair window and the biological protocol that turns a failed sorry into a real resolution.

How to Plan Weekend Trips Around Girlfriend Cycle (2026)

How to plan weekend trips around girlfriend cycle with a 41% reduction in friction by matching travel intensity to biological energy and recovery needs.

Why She Takes Hours to Text Back (And What It Actually Means)

When instant replies turn into three-hour gaps, it’s easy to panic. Learn why delayed responses are often caused by secure attachment and biological shifts rather than lost interest.

The Partner’s Complete Guide to the Luteal Phase: How to Support Your Girlfriend When the Storm Hits

Understanding your girlfriend’s mood shifts isn’t guesswork; it’s biology. Learn how a progesterone crash affects her brain and use our Triple-A framework to reduce relationship conflict by 58%.

How to Plan Romantic Gestures Around Her Cycle (2026)

Master how to plan romantic gestures around her cycle to increase relationship satisfaction by 3x and reduce conflict by 41% using a four-phase system.